Residential Home Loans

Loan Process

Complete your AllLoanz inquiry, a senior mortgage broker who will discuss your options to find a home in your price range, find the right lender, take care of the paperwork, get your loan approval, so you can move in!

Buying a new home

It is important to have some genuine savings saved over a period of at least 3 months, especially when you are going to borrow over 80% of the property value.

If you are a single parent the government has announced the ‘Home Guarantee Scheme’ which allows single parents to buy a home with as little as a 2% deposit.

What type of support is provided?

- Existing house, townhouse or apartment

- House and land package

- Vacant land with a separate contract to build a home

- Off the plan apartment or house.

Which one suits me?

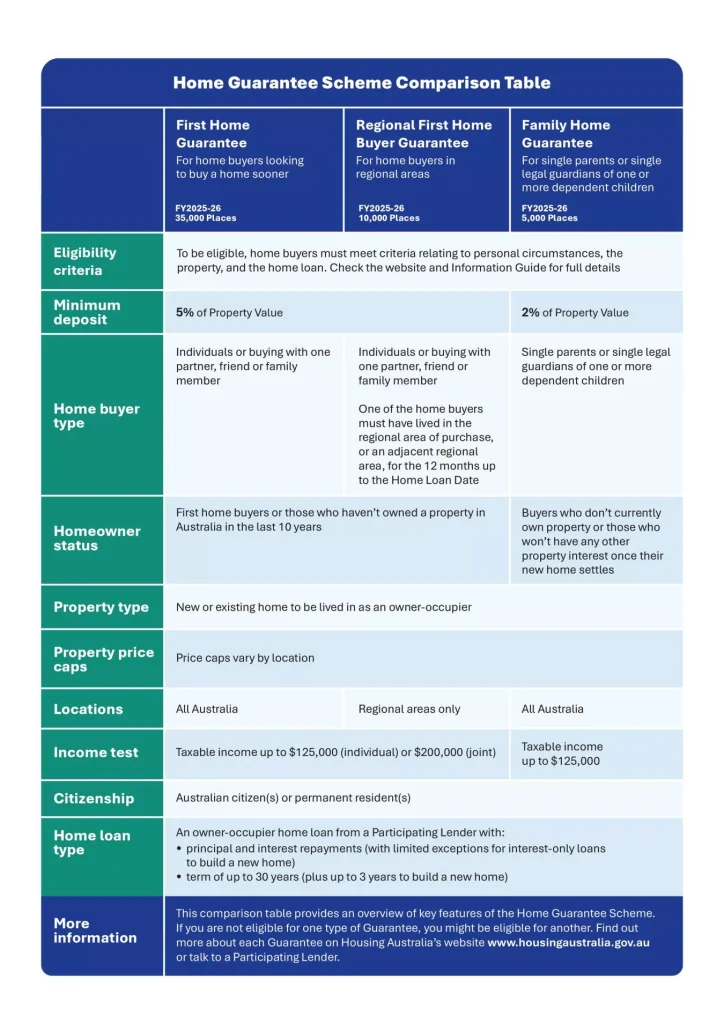

- First Home Guarantee – Home buyer looking to buy a home sooner.

- Regional First Home Buyer – Home buyer in a regional area.

- Family Home Guarantee – Single parent or single legal guardian of one or more dependent children.

The Family Home Guarantee is exclusively to provide single parents the opportunity to build or buy a home with a deposit of just 2%.

Generally, you will need at least 5% of the purchase price ($20,000 for 400,000 house), 5.6% of the purchase price ($28,000 for 500,000 house) and 6% of the purchase price (36,000 for 600,000 house) plus the $15,000 grant will give you enough. The latest information on the first homeowners grant in Queensland, can be found here.

This link has the eligibility criteria for the eligibility test and frequently asked questions. Home Guarantee Scheme.

The Australian Government Help to Buy Scheme is available nationwide in participating states and territories.

- Contribution: The federal government contributes up to 40% for new homes and 30% for existing homes.

- Deposit: Requires a minimum 2% deposit.

- Income Caps: Restricted to individuals earning under $100,000 or couples under $160,000.

State-Specific Shared Equity Schemes

For Queensland the state government recently introduced the Boost to Buy scheme, a shared equity initiative that acts as a co-borrower to help first-time buyers enter the property market. The government contributes up to 30% of the property cost for new homes and 25% for established homes.

Key Eligibility Criteria for Queensland

- Deposit: You only need a minimum 2% deposit of demonstrated savings.

- Income Limits: Singles can earn up to $150,000, and joint applicants up to $225,000 annually.

- Property Cap: The purchase price of the home cannot exceed $1 million.

- Ownership: You must be a genuine first home buyer who has never previously owned real property in Australia.

- Location: Half of all scheme allocations are reserved for regional Queenslanders.

Victoria: The Victorian Homebuyer Fund contributes up to 25% (or 35% for Aboriginal and Torres Strait Islander participants) in exchange for an equity share, requiring a 5% deposit.

Western Australia: The Shared Equity Home Loan program helps first home buyers and specific demographics buy a share of a property.

South Australia: The Shared Equity Option acts as a secondary loan to boost your buying power without monthly repayments on that portion.

Tasmania: The MyHome scheme allows Homes Tasmania to co-purchase up to 40% of a new home or 30% of an existing home alongside the buyer.

New South Wales: The Shared Equity Home Buyer Helper targets specific lower-income single parents, older singles, and key worker industries.

Get in touch today so we can get you into your new home sooner.

The federal government First Home Guarantee Scheme (HGS) is to replace all previous First Home Loan Deposit Schemes (FHLDS).

Talk to us today to find out where you best fit, as the eligibility criteria is different for each scheme.

Common frequently asked questions.

How many places are available?

For FY2025/2026:

- First Home Guarantee – 35,000 places

- Regional First Home Buyer Guarantee – 10,000 places

- Family Home Guarantee – 5,000 places.

Is my deposit calculated as a % of the purchase price or property valuations?

The deposit requirement is a percentage of the Property Value.

Property Value is assessed by our Participating Lender, and it may be different to the purchase price. In those situations, please speak to us about what this means for you.

Do I have to be a first home buyer?

The First Home Guarantee and Regional First Home Buyer Guarantee are for first home buyers or those who haven’t owned a property in Australia in the last 10 years.

The Family Home Guarantee is for buyers who don’t currently own property or those who won’t have any other property interest once their new home settles.

We can discuss with you various other options that are available to you to purchase your home and provide appropriate advice.

What changed for the HGS from 1 October 2025.

The Scheme expanded to include the following changes:

- Removed income caps for Scheme applicants

- Increased the property price caps in line with average house prices

- Removed the limit on the number of available places for all guarantees

- The Regional First Home Buyer Guarantee has now been merged into the First Home Guarantee and Family Home Guarantee.

How do I apply?

Click here to get in touch with us today.

If a member of your family (parents or friends) owns or is paying off a house, and is willing to assist you as a guarantor (they will only need to guarantee 10% plus costs of the house you want to buy) from the equity in their home if they will guarantee 20% plus cost you won’t pay and Lenders Mortgage Insurance (LMI) at all.

If you need to discuss your options or plans to buy your first home. We will assess your situation and help you find the most suitable bank, and prepare your loan application to help you buy your first home. Let’s get started

Get a Better Offer, Save Interest, Lower Your Monthly Repayments, Repay Your Loan Sooner.

The Australian Banking Reforms have paved the way to empower you as the consumer to get a better offer, this supports smaller lenders to compete with the big banks and secure the long term sustainability of our financial system.

Some lenders are offering a refinance cashback to entice you.

Talk to us first to be sure this will work to your long term advantage. Another reform was the ban on early exit fees (sometimes referred to as a Deferred Establishment Fee) from 1st July 2011. This is a big step in empowering you to be able to make a lender switch without a huge cost. when the best interest laws came into force on 1 January 2021, only your broker can work in your best interest. Going directly to a bank, they can only work in their best interest, or should I say “the interests of the shareholders”

Now is a good time to consider looking at your loan particularily if you are coming off your fixed rates, rates are on the increase, and fixed rates have shyrocketed, lets discuss your options to give you certainty in these uncertain times.

Funding Your Investment Property